Model Evaluation¶

Goals¶

- Minimize bias

- Minimize variance

- Minimize generalization gap

Guidelines¶

- Always check if your model is able to learn from a synthetic dataset where you know the underlying data-generating process

- Always evaluate model with different random seeds to ensure accurate result

- Group by random seed and check for discrepancies

- Metrics computed from test set may not be representative of the true population

- Always look at multiple metrics; never trust a single one alone

- false positives and false negatives are seldom equivalent

- understand the problem to known the right tradeoff

- Always monitor the worst-case prediction

- Maximum loss

- 95th percentile loss

Baseline/Benchark models¶

Always establish a baseline

- Basic/Naive/Dummy predictions

- Regression

- Mean

- Max

- Min

- Random

- Classification

- Mode

- Random

- Time series specific

- Persistence

- \(\hat y_{t+h} = y_t\)

- Latest value available

- Great for short horizons

- Climatology

- \(\hat y_{t+h} = \bar y_{i \le t}\)

- Average of all observations until present

- Great for short horizons

- Combination of Persistence and Climatology

- \(\hat y_{t+h} = \beta_1 y_t + \beta_2 \bar y_{i \le t}\)

- Lag: \(\hat y_{t+h} = y_{t-k}\)

- Seasonal Lag: \(\hat y_{t+h} = y_{t+h-m}\)

- Moving average

- Exponential average

- Human Level Performance

- Literature Review

- Performance of older system

Significance¶

All the evaluation should be performed relative to the baseline.

For eg: Relative RMSE = RMSE(model)/RMSE(baseline), with “good” threshold as 1

Probabilistic Evaluation¶

Now, we need to see if any difference in accuracy across models/hyperparameters is statistically-significant, or just a matter of chance - Try different seeds and see the range; this range is purely due to randomness

Summary Statistics: Don’t just look at the mean evaluation metric of the multiple splits; also get the uncertainty associated with the validation process.

It is invalid to use a standard hypothesis test - such as a T-test - across the different folds of a cross-validation, as the runs are not independent. - It is acceptable for a fixed test set - Std obtained in model performance from cross-validation is standard error of mean estimate - Std obtained in model performance from cross-validation is standard error of mean estimate - True standard deviation is no of folds x SE

Hence, treat the metrics across the folds as a a distribution - For regression: chi squared - For classification: binomial

- Standard error of accuracy estimate

- Standard deviation

- Quantiles

- VaR

Bessel’s Correction¶

- where

- \(n=\) no of samples

- \(k=\) no of parameters

- \(e=\) no of intermediate estimates (such as \(\bar x\) for variance)

- Do not perform this on metrics which are already corrected for degree of freedom (such as \(R^2_\text{adj}\))

- Modify accordingly for squares/root metrics

Regression Evaluation¶

| Metric | Formula | Unit | Range | Preferred Value | Signifies | Advantages ✅ | Disadvantages ❌ | Comment |

|---|---|---|---|---|---|---|---|---|

| \(R^2\) (Coefficient of Determination) | \(1 - \text{RSE}\) | Unitless | \([0, 1]\) | \(1\) | Proportion of changes in dependent var explained by regressors. Proportion of variance in \(y\) explained by model wrt variance explained by mean Demonstrates ___ of regressors - Relevance - Power - Importance | Cannot use to compare same model on different samples, as it depends on variance of sample Susceptible to spurious regression, as it increases automatically when increasing predictors | ||

| Adjusted \(R^2\) | \(1 - \left[\dfrac{(n-1)}{(n-k-1)} (1-R^2)\right]\) | Unitless | \([0, 1]\) | \(1\) | Penalizes large number of predictors | |||

| Accuracy | \(100 - \text{MAPE}\) | % | \([0, 100]\) | \(100 \%\) | ||||

| \(\chi^2_\text{reduced}\) | \(\dfrac{\chi^2}{n-k} = \dfrac{1}{n-k}\sum \left( u_i/\sigma_i \right)^2\) | \([0, \infty]\) | \(1\) | \(\approx 1:\) Good fit \(\gg 1:\) Underfit/Low variance estimate \(\ll 1:\) Overfit/High variance estimate | ||||

| Spearman’s Correlation | \(\dfrac{ r(\ rg( \hat y), rg(y) \ ) }{ \sigma(\ rg(\hat y) \ ) \cdot \sigma( \ rg(y) \ ) }\) | Unitless | \([-1, 1]\) | \(1\) | Very robust against outliers Invariant under monotone transformations of \(y\) | |||

| DW (Durbin-Watson Stat) | \(> 2\) | Confidence of error term being random process | Not appropriate when \(k>n\) | Similar to \(t\) or \(z\) value If \(R^2 >\) DW Statistic, there is Spurious Regression | ||||

| AIC Akaike Information Criterion | \(-2 \ln L + 2k\) | \(0\) | Leave-one-out cross validation score | Penalizes predictors more heavily than \(R_\text{adj}^2\) | For small values of \(n\), selects too many predictors Not appropriate when \(k>n\) | |||

| AIC Corrected | \(\text{AIC} + \dfrac{2k(k+1)}{n-k-1}\) | \(0\) | Encourages feature selection | |||||

| BIC/SBIC/SC (Schwarz’s Bayesian Information Criterion) | \(-2 \ln L + k \ln n\) | \(0\) | Penalizes predictors more heavily than AIC | |||||

| HQIC Hannan-Quinn Information Criterion | \(-2 \ln L + 2k \ln \vert \ln n \vert\) | \(0\) | ||||||

| Calibration |  | |||||||

| Sharpness |  |

Probabilistic Evaluation¶

You can model the error such as MAE as a \(\chi^2\) distribution with dof = \(n-k\)

The uncertainty can be obtained from the distribution

Spurious Regression¶

Misleading statistical evidence of a relationship that does not truly exist

Occurs when we perform regression between

- 2 independent variables

and/or

- 2 non-stationary variables

(Refer econometrics)

You may get high \(R^2\) and \(t\) values, but \(u_t\) is not white noise (it is non-stationary)

\(\sigma^2_u\) becomes infinite as we go further in time

Classification Evaluation¶

There is always a tradeoff b/w specificity and sensitivity

| Metric | Formula | Preferred Value | Unit | Range | Meaning |

|---|---|---|---|---|---|

| Entropy of each classification | \(H_i = -\sum \hat y \ln \hat y\) | \(\downarrow\) | \([0, \infty)\) | Uncertainty in a single classification | |

| Mean Entropy | \(H_i = -\sum \hat y \ln \hat y\) | Uncertainty in classification of entire dataset | |||

| Accuracy | \(1 - \text{Error}\) \(\dfrac{\text{TP + TN}}{\text{TP + FP + TN + FN}}\) | \(\uparrow\) | % | \([0, 100]\) | \(\dfrac{\text{No of Correct Predictions}}{\text{Total no of predictions}}\) |

| Error | \(\dfrac{\text{FP + FN}}{\text{TP + FP + TN + FN}}\) | \([0, 1]\) | \(\downarrow\) | \(\dfrac{\text{Wrong Predictions}}{\text{No of predictions}}\) | |

| F Score F1 Score F-Measure | \(\dfrac{2}{\dfrac{1}{\text{Precision}} + \dfrac{1}{\text{Recall}}}\) \(2 \times \dfrac{P \times R}{P + R}\) | \(\uparrow\) | Unitless | \([0, 1]\) | Harmonic mean between precision and recall Close to lower value |

| ROC-AUC Receiver-Operator Characteristics-Area Under Curve | Sensitivity vs (1-Specificity) = (1-FNR) vs FPR | \(\uparrow\) | Unitless | \([0, 1]\) | AUC = Probability that algo ranks a +ve over a -ve Robust to unbalanced dataset |

| Precision PPV/ Positive Predictive Value | \(\dfrac{\textcolor{hotpink}{\text{TP}}}{\textcolor{hotpink}{\text{TP}} + \text{FP}}\) | \(\uparrow\) | Unitless | \([0, 1]\) | Indicates how many +ve predictions were correct predictions |

| Recall Sensitivity True Positive Rate | \(\dfrac{\textcolor{hotpink}{\text{TP}}}{\textcolor{hotpink}{\text{TP}} + \text{FN}}\) | \(\uparrow\) | Unitless | \([0, 1]\) | Out of actual +ve values, how many were correctly predicted as +ve |

| Specificity True Negative Rate | \(\dfrac{\textcolor{hotpink}{\text{TN}}}{\textcolor{hotpink}{\text{TN}} + \text{FP}}\) | \(\uparrow\) | Unitless | \([0, 1]\) | Out of actual -ve values, how many were correctly predicted as -ve |

| NPV Negative Predictive Value | \(\dfrac{\textcolor{hotpink}{\text{TN}}}{\textcolor{hotpink}{\text{TN}} + \text{FN}}\) | Unitless | \([0, 1]\) | Out of actual -ve values, how many were correctly predicted as -ve | |

| \(F_\beta\) Score | \(\dfrac{(1 + \beta^2)}{{\beta^2}} \times \dfrac{P \times R}{P + R}\) | \(\uparrow\) | Unitless | [0, 1] | Balance between importance of precision/recall |

| FP Rate | \(\begin{aligned}\alpha &= \dfrac{\textcolor{hotpink}{\text{FP}}}{\textcolor{hotpink}{\text{FP}} + \text{TN}} \\ &= 1 - \text{Specificity} \end{aligned}\) | \(\downarrow\) | Unitless | \([0, 1]\) | Out of the actual -ve, how many were misclassified as Positive |

| FN Rate | \(\begin{aligned}\beta &= \dfrac{\textcolor{hotpink}{\text{FN}}}{\textcolor{hotpink}{\text{FN}} + \text{TP}} \\ &= 1 - \text{Sensitivity} \end{aligned}\) | \(\downarrow\) | Unitless | \([0, 1]\) | Out of the actual +ve, how many were misclassified as Negative |

| Balanced Accuracy | \(\frac{\text{Sensitivity + Specificity}}2{}\) | Unitless | |||

| MCC Mathews Correlation Coefficient | \(\dfrac{\text{TP} \cdot \text{TN} - \text{FP}\cdot \text{FN} }{\sqrt{(\text{TP}+\text{FP})(\text{TP}+\text{FN})(\text{TN}+\text{FP})(\text{TN}+\text{FN})}}\) | \(\uparrow\) | Unitless | \([-1, 1]\) | 1 = perfect classification 0 = random classification -1 = perfect misclassification |

| Markdedness | PPV + NPV - 1 | ||||

| Brier Score Scaled | |||||

| Nagelkerke’s \(R^2\) | |||||

| Hosmer-Lemeshow Test | Calibration: agreement b/w obs and predicted |

Graphs¶

| Graph | Preferred | ||

|---|---|---|---|

| Error Rate |  | ||

| ROC Curve |  | How does the classifier compare to a classifier that predicts randomly with \(p=\text{TPR}\) How well model can discriminate between \(y=0\) and \(y=1\) | Top-Left At least higher than 45deg line |

| Calibration Graph |  | Create bins of different predicted probabilities Calculate the fraction of \(y=1\) for each bin Confidence intervals (more uncertainty for bins with fewer samples) Histogram showing fraction of samples in each bin | Along 45deg line |

| Confusion Probabilities |  |

Tradeoff for Threshold¶

Probabilistic Evaluation¶

For simple metrics that rely on counting successes, such as accuracy, sensitivity, PPV, NPV - the sampling distribution can be deduced from a binomial law - uncertainty via Proportion Testing

- \(n=\) Validation set size

- = \(\sum \limits_i^k n_\text{fold}\)

- \(\hat p =\) Average Accuracy of classifier = Estimated proportion

- \(= \dfrac{1}{k} \sum \limits_i^k \text{Accuracy}_\text{fold}\)

Decision Boundary¶

Plot random distribution of values

For eg:

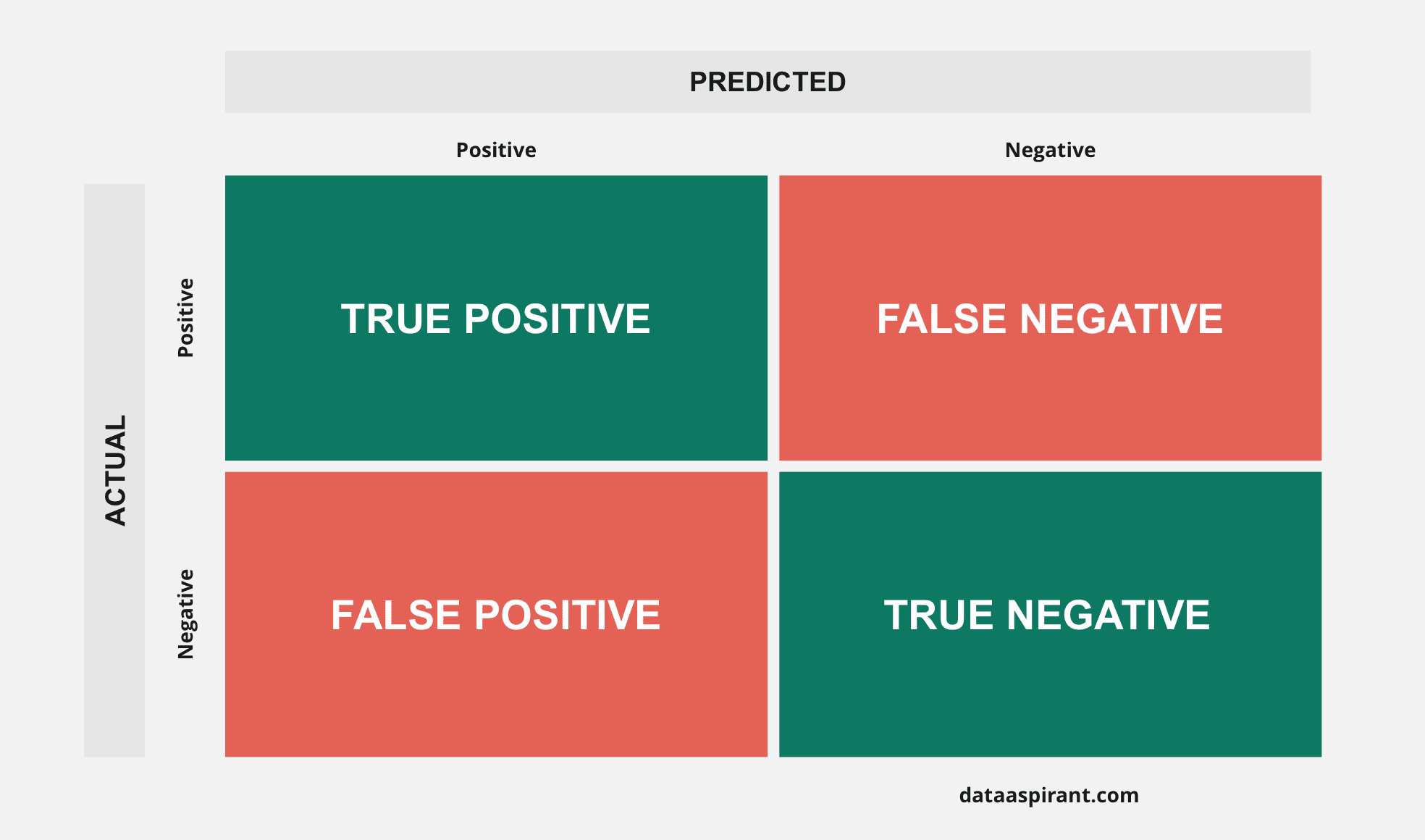

Confusion Matrix¶

\(n \times n\) matrix, where \(n\) is the number of classes

Binary Classification¶

Multi-Class Classification¶

Confusion Matrix with respect to A

| A | B | C | |

|---|---|---|---|

| A | TP | FN | FN |

| B | FP | TN | TN |

| C | FP | TN | TN |

Classification Accuracy Measures¶

Jacquard Index¶

Multi-Class Averaging¶

| Micro-Average | All samples equally contribute to average | \(\dfrac{1}{C}\sum_{c=1}^C \dfrac{\dots}{\dots}\) |

| Macro-Average | All classes equally contribute to average | \(\dfrac{\sum_{c=1}^C \dots}{\sum_{c=1}^C \dots}\) |

| Weighted-Average | Each class’ contribution to average is weighted by its size | \(\sum_{c=1}^C \dfrac{n_c}{n} \dfrac{\dots}{\dots}\) |

Inspection¶

| Inspection | Identify |

|---|---|

| Error Analysis | Systematic errors |

| Bias-Variance Analysis | General errors |

Error Analysis¶

Residual Inspection

Perform all the inspection on

- train and dev data

- externally-studentized residuals, to correct for leverage

There should be no explainable unsystematic component

- Symmetric distribution for values of error terms for a given value \(x\)

- Not over time/different values of \(x\)

- This means that

- you have used up all the possible factors

- \(u_i\) only contains the non-systematic component

| Ensure | Meaning | Numerical | Graphical | Implication if violated | Action if violated |

|---|---|---|---|---|---|

| Random residuals | - No relationship between error and independent variables - No relationship between error and predictions - If there is correlation, \(\exists\) unexplained system component | Normality test \(E(a \vert b) = 0\) \(r(a, b) = 0\) \(\text{MI}(a, b) = 0\) \(a \in [u, \vert u \vert , u^2, \log \vert u \vert]\) \(b \in [ c, \vert c \vert , c^2, \log \vert c \vert]\) \(c \in [x_j, y, \hat y]\) | Q-Q Plot Histogram Parallel coordinates plot | ❌ Unbiased parameters | Fix model misspecification |

| No autocorrelation | - Random sequence of residuals should bounce between +ve and -ve according to a binomial distribution - Too many/few bounces may mean that sequence is not random No autocorrelation between \(u_i\) and \(u_j\) | \(r(u_i, u_j \vert x_i, x_j )=0\) Runs test DW Test | Sequence Plot of \(u_i\) vs \(t\) Lag Plot of \(u_i\) vs \(u_j\) | ✅ Parameters remain unbiased ❌ MSE estimate will be lower than true residual variance Properties of error terms in presence of \(AR(1)\) autocorrelation - \(E[u_i]=0\) - \(\text{var}(u_i)= \sigma^2/(1-\rho^2)\) - \(r(u_i, u_{i-p}) = \rho^p \text{var}(u_i) = \rho^p \sigma^2/(1-\rho^2)\) | Fix model misspecification Incorporate trend Incorporate lag (last resort) Autocorrelation analysis |

| No effect of outliers | Outlier removal/adjustment | ||||

| Low leverage & influence of each point | Data transformation | ||||

| Homoscedasticity (Constant variance) | \(\sigma^2 (u_i \vert x_i) = \text{constant}\) should be same \(\forall i\) | Weighted regression | |||

| Error in input variables | Total regression | ||||

| Correct model specification | Model building | ||||

| Goodness of fit | - MLE Percentiles - Kolmogorov Smirnov | ||||

| Significance in difference in residuals for models/baselines | Ensure that all the models are truly different, or is the conclusion that one model is performing better than another due to chance | Comparing Samples |

Why is this important?¶

For eg: Running OLS on Anscombe’s quartet gives

- same curve fit for all

- Same \(R^2\), RMSE, standard errors for coefficients for all

But clearly the fit is not equally optimal

- Only the first one is acceptable

- Model misspecification

- Outlier

- Leverage

which is shown in the residual plot

Aggregated Inspection¶

- Aggregate the data based on metadata

- Evaluate metrics on groups

where \(g()\) is the group, which can be \(x_{ij}, y_i\) or combination of these

- Image blurry/flipped/mislabelled

- Gender

- Age

- Age & Gender

Diebold-Mariano Test¶

Determine whether predictions of 2 models are significantly different

Basically the same as Comparing Samples for residuals

Bias-Variance Analysis¶

Evaluation Curves¶

Related to Interpretation

- Always look at all curves with uncertainties wrt each epoch, train, hyper-parameter value.

- The uncertainty in-sample and out-sample should also be similar

- If train set metric uncertainty is small and test set metric uncertainty is large, this is bad even if the average loss metric is same

| Learning Curve | Loss Curve | Validation Curve | |

|---|---|---|---|

| Loss vs | Train Size | Epochs | Hyper-parameter value |

| Comment | Train Error increases with train size, because model overfits small train datasets | ||

| Purpose: Detect | Bias Variance Utility of adding more data | Optimization problems Undertraining Overtraining | Model Complexity Optimal Hyperparameters |

| No retraining | ❌ | ✅ | ❌ |

| No extra computation | ❌ | ✅ | ❌ |

| Speed up | If this takes too long, don't evaluate loss/accuracy every epoch - train_eval_every: saving results- dev_eval_every: forward pass, saving results |

Learning Curve¶

Based on the slope of the curves, determine if adding more data will help

| Conclusion | |

|---|---|

| High Bias (Underfitting) |

| High Variance (Overfitting) |

| High Bias High Variance |

Loss Curve¶

Same Model, Variable Learning Rate¶

Validation Curve¶

Neural Network Distributions¶

| Recommended Value | ||

|---|---|---|

| Activation forward-pass distributions | \(N(0, 1)\) | |

| Activation gradient distributions | \(N(0, 1)\) | |

| Parameter forward-pass weight distributions | \(N(0, 1)\) | |

| Parameter gradient distributions | \(N(0, 1)\) | |

| Parameter gradient std:weights magnitude std | \(1\) | |

| Parameter update std:weights magnitude std | \(10^{-3}\) |

Avoids

- Saturation

- Exploding

Example Plot¶

Object Detection¶

| Metric | Range | Preferred Value | |

|---|---|---|---|

| mAP mean Average Precision | Mean of Average precision across each class | \([0, 1]\) | \(1\) |

| IOU Intersection Over Union | \(\frac{\text{Area}(T \cap P)}{\text{Area}(T \cup P)}\) - True bounding box = \(T\) - Proposed bounding box = \(P\) | \([0, 1]\) | \(1\) \(> 0.9\) Excellent \(> 0.7\) Good o.w: Poor |

IDK¶