03 Process of Accounting

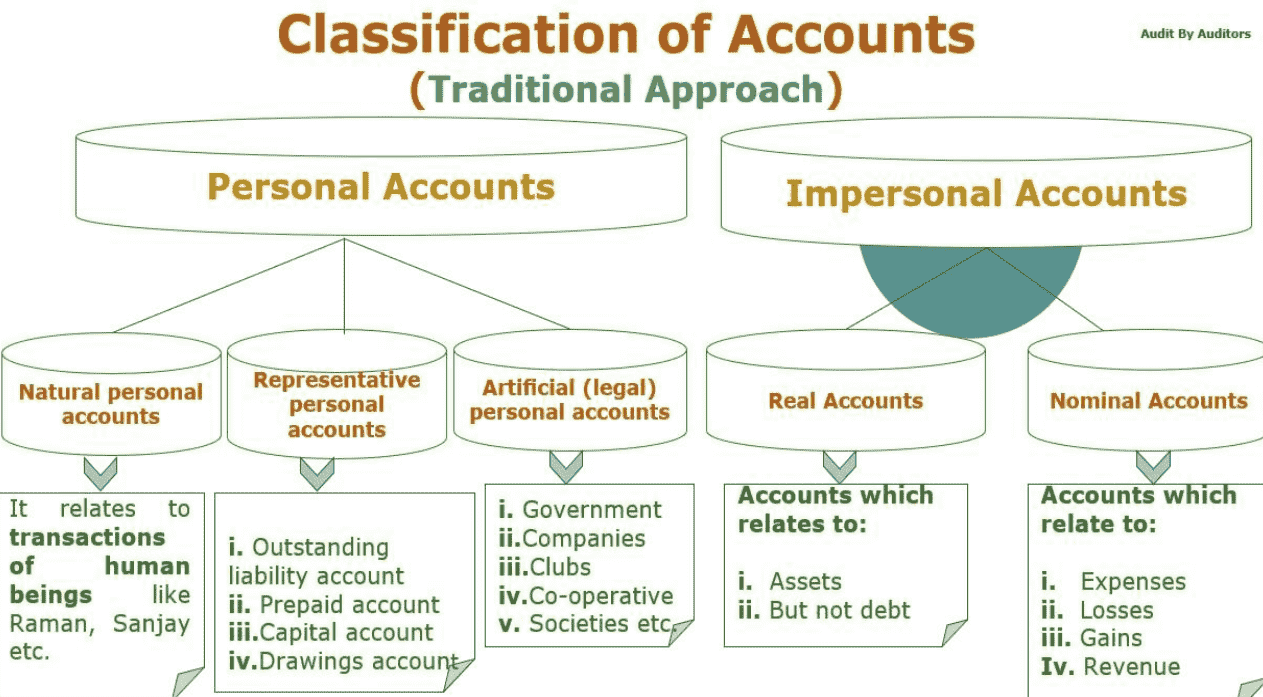

Types of Accounts¶

| Account | Debit | Credit |

|---|---|---|

| Personal | Receiver | Giver |

| Real | What comes in | What goes out |

| Nominal | Expenses & Losses | Income & Gains |

Accounting Equation¶

| Assets + Expenses | Liabilities + Equity + Revenue | |

|---|---|---|

| Increases | Dr. | Cr. |

| Decreases | Cr. | Dr. |

Accounting Cycle¶

flowchart LR

sd[Source<br/>Documents] -->

|Journalize| Journal -->

|Posting| Ledger -->

tb[Trial<br/>Balance]-->

fs

subgraph fs[Financial<br/>Statements]

direction LR

bs[Balance<br/>Sheet]

pl[Profit-Loss/<br/>Income]

cf[Cashflow]

endJournal¶

Record of transactions, regardless of income, expenses, etc

| Date | Particulars | Debit(Dhs) | Credit(Dhs) |

|---|---|---|---|

| 2022-01-01 | Cash A/C Dr. | 20,000 | |

| To Capital A/C | 20,000 | ||

| (Being commencement of business) |

To means: Debitor(Dr.) is indebted to Creditor(Cr.)

Purpose¶

- provides permanent record

- provides information of debit and credit in an entry and an explanation

- reduces the possibility of error as both aspects of a business transaction are written side by side

Compound Journal Entries¶

| Date | Particulars | Debit (Dhs) | Credit(Dhs) |

|---|---|---|---|

| 2022-01-01 | Cash A/C Dr. | 20,000 | |

| To Electricity Company | 10,000 | ||

| To Water Company | 10,000 | ||

| (Expenditure on Utilities) |

Transactions involving Discount A/C are always compound journal entries

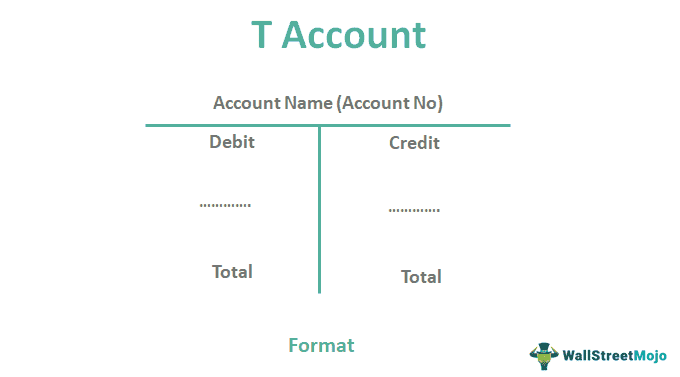

Ledger¶

Summary statement of all the transactions relating to a person, asset, expense or income which have taken place during a given period of time and shows their net effect

- Debit side = Receipts side

- Credit side = Payment side

It is in a ‘T’ form

| Dr | < Account Name > | Cr. | ||||

|---|---|---|---|---|---|---|

| Date | Particulars | Amount | Date | Particulars | Amount | |

| 2022-01-01 | To Credit A/C | 2022-01-01 | By Debit A/C | |||

| Total | \(d\) | Total | \(c\) |

Overage Balance¶

Overage = surplus of debit/credit

| Symbol | Meaning |

|---|---|

| C/D | Carried Down |

| B/D | Brought Down |

| Case | Dr | Cr |

|---|---|---|

| \(d>c\) | To Balance B/D | By Balance C/D |

| \(d<c\) | To Balance C/D | By Balance B/D |

Trial Balance¶

List of overages of the ledger accounts at a particular point of time

The selected side (debit/credit) is the one having the amount brought down to next period.

If everything is right, the trial balance should result in

\[ \sum \text{Debit Overages} = \sum \text{Credit Overages} \]

| S. No | Name of A/C | Debit (Dhs) | Credit (Dhs) |

|---|---|---|---|

| \(a\) | |||

| \(b\) | |||

| Total | \(k\) | \(k\) |