Time Series Processes¶

Time Series¶

Observation of random variable ordered by time

Time series variable can be

- Time series at level (absolute value)

- Difference series (relative value)

- First order difference \(\Delta y_t = y_t - y_{t-1}\)

- Called as ‘returns’ in finance

- Second order difference \((\Delta y_t)_2 = \Delta y_t - \Delta y_{t-1}\)

Univariate Time Series¶

Basic model only using a variable’s own properties like lagged values, trend, seasonality, etc

Why do we use different techniques for time series?¶

This is due to

- behavioral effect

- history/memory effect

- Medical industry always looks at the records of your medical history

- Inertia of change

- Limited data

Components of Time Series Processes¶

| Characteristic | Frequency | ||

|---|---|---|---|

| Auto-Correlation | |||

| Level | Average value of series | ||

| Trend | Gradual | Low | |

| Seasonality | Daily, Weekly, Monthly | ||

| Cycles | > 1 year | Economy cycle | |

| Holidays | Eid, Christmas | ||

| Drift | Exogeneous | ||

| Structural Break | |||

| Shocks | |||

| Noise | Random | High |

Auto-correlation¶

High possibility of auto-correlation

Sometimes just auto-correlation is enough to learn the values of a value

If we take \(j\) lags,

Generally, \(i>j \implies \beta_i < \beta_j\)

Impact of earlier lags is lower than impact of recent lags

Shock¶

‘Shock’ is an abrupt/unexpected deviation(inc/dec) of the value of a variable from its expected value

This incorporates influence of previous disturbance

They cause a structural change in our model equation. Hence, we need to incorporate their effect.

Basically, shock is basically \(u_t\) but it is fancily called as a shock, because they are large \(u\)

Can be

| Temporary | Permanent | |

|---|---|---|

| Duration | Short-term | Long-Term |

| Causes structural change | ||

| Examples | Change in financial activity due to Covid | Change in financial activity due to 2008 Financial Crisis |

| Heart rate change due to minor stroke Heart rate change due to playing | Heart rate change due to major stroke Heart rate change due to big injury | |

| Goals scored change due to small fever | Goals scored change due to big injury |

Model becomes

Structural Breaks¶

Permanent change in the variable causes permanent change in relationship

We can either use

- different models before and after structural break

- binary ‘structural dummy variable’ to capture this effect

For eg, long-term injury

Trend¶

Tendency of time series to change at a certain expected rate.

Trend can be

- deterministic/systematic (measurable)

- random/stochastic (not measurable \(\implies\) cannot be incorporated)

For eg: as age increases, humans have a trend of

- growing at a certain till the age of 20 or so

- reducing heart rate

Model becomes

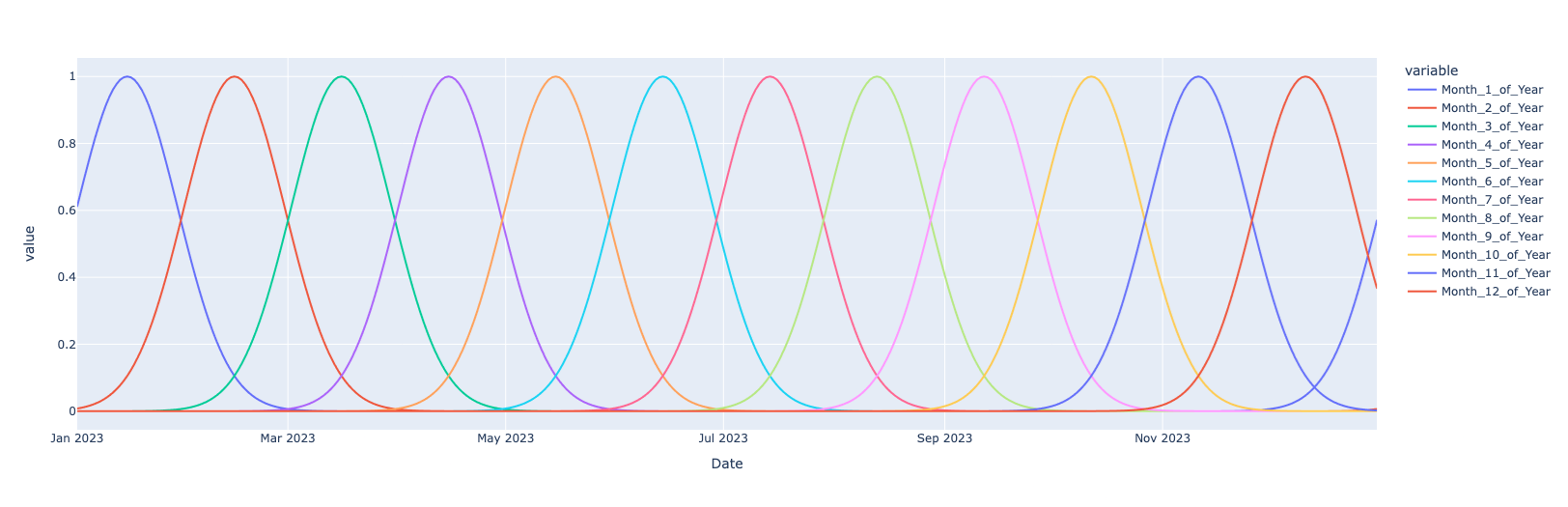

Seasonality/Periodicity¶

Tendency of a variable to change in a certain manner at regular intervals.

For eg

- demand for woolen clothes is high every winter

- demand for ice cream is high every summer

Finance industry has ‘anomalies’

Two ways to encode

| Type | Advantage | Disadvantage | Example | \(S\) | ||

|---|---|---|---|---|---|---|

| Binary | Simple | Unrealistic | Dummy | \(\{0, 1\}\) | ||

| Continuous | Realistic | Complex | Cyclic Linear Basis | \(\exp{\left[\frac{- 1}{2 \alpha^2} (x_i - \text{pivot})^2\right]}\) - Pivot is the center of the curve | Preferred, as more control over amplitude and bandwidth |  |

| Fourier series | \(\alpha \cos \left(\frac{2 \pi}{\nu} + \phi \right) + \beta \sin \left( \frac{2 \pi}{\nu} + \phi\right)\), where \(\nu =\) Frequency of seasonality, and \(\phi\) is the offset - Quarterly = 4 - Monthly = 12 |

Volatility¶

Annualized standard deviation of change of a random variable

Measure of variation of a variable from its expected value

If the variance is heteroskedastic (changes over time), the variable is volatile

Lag Terms¶

Here, \(\rho_1\) and \(\rho_2\) are partial-autocorrelation coefficient of \(y_{t-1}\) and \(y_{t-2}\) on \(y_t\)

Here, \(\rho_1\) is total autocorrelation coefficient of \(y_{t-2}\) on \(y_t\)

We choose the number of lags by trial-and-error and checking which coefficients are significant (\(\ne 0\))

Stochastic Data-Generating Processes¶

Stochastic process is a sequence of random observations indexed by time

Markov Chain¶

Stochastic process where effect of past on future is summarized only by current state $$ P(y_{t+1} = a \vert x_0, x_1, \dots x_t) = P(x_{t+1} = a \vert x_t) $$ If possible values of \(x_i\) is a finite set, MC can be represented as a transition probability matrix

Martingale¶

Stochastic processes which are a “fair” game $$ E[y_{t+1} \vert y_t] = y_t $$ Follow optimal stopping theorem

Subordinated¶

Stationarity¶

| Type | Meaning |

|---|---|

| Stationary | Constant mean: \(E(y_t) = \mu\) Constant variance: \(\text{Var}(y_t) = \sigma^2\) |

| Covariance Stationary | Constant mean: \(E(y_t) = \mu\) Constant variance: \(\text{Var}(y_t) = \sigma^2\) Constant auto-covariance: \(\text{Cov}(y_{t+h}, y_t) = \gamma(\tau)\) |

| Non-Stationary | Will have either one/both of the following - Mean at each time period is different across all time periods - Mean of distribution of possible outcomes corresponding to each time period is different - Variance at each time period is different across all time periods - Variance of distribution of possible outcomes corresponding to each time period is different We need to transform this somehow, as OLS and GMM cannot be used for non-stationary processes, because the properties of OLS are violated - heteroskedastic variance of error term |

Types of Stochastic Processes¶

Consider \(u_t = N(0, \sigma^2)\)

| Process | Characteristics | \(y_t\) | Comments | Mean | Variance | Memory | Example |

|---|---|---|---|---|---|---|---|

| White Noise | Stationary | \(u_t\) | PAC & TAC for each lag = 0 | 0 | \(\sigma^2\) | None | If a financial series is a white noise series, then we say that the ‘market is efficient’ |

| Ornstein Uhlenbeck Process/ Vasicek Model | Stationary Markov chain | \(\beta_1 y_{t-1} + u_t; \ 0 < \vert \beta_1 \vert < 1\) | Series has Mean-reverting Earlier past is less important compared to recent past. Less susceptible to permanent shock Series oscilates | 0/non-zero | \(\sigma^2\) | Short | GDP growth Interest rate spreads Real exchange rates Valuation ratios (divides-price, earnings-price) |

| Covariance Stationary | \(y_t = V_t + S_t\) (Wold Representation Theorem) \(V_t\) is a linear combination of past values of \(V_t\) with constant coefficients \(S_t = \sum \psi_i u_{t-i}\) is an infinite moving-average process of error terms, where \(\psi_0=1, \sum \psi_i^2 < \infty\); \(\eta_t\) is linearly-unpredictable white noise and \(u_t\) is uncorrelated with \(V_t\) | ||||||

| Simple Random Walk | Non-Stationary Markov chain Martingale | \(\begin{aligned} &= y_{t-1} + u_t \\ &= y_0 + \sum_{i=0}^t u_i \end{aligned}\) | PAC & TAC for each lag = 0 \(y_{t+h} - y_t\) has the same dist as \(y_h\) | \(y_0\) | \(t \sigma^2\) | Long | |

| Explosive Process | Non-Stationary | \(\beta_1 y_{t-1} + u_t; \ \vert \beta_1 \vert > 1\) | |||||

| Random Walk w/ drift | Non-Stationary | \(\begin{aligned} &= \beta_0 + y_{t-1} + u_t \\ &= t\beta_0 + y_0 + \sum_{i=0}^t u_i \end{aligned}\) | \(t \beta_0 + y_0\) | \(t \sigma^2\) | Long | ||

| Random Walk w/ drift and deterministic trend | Non-Stationary | \(\begin{aligned} &= \beta_0 + \beta_1 t + y_{t-1} + u_t \\ &= y_0 + t \beta_0 + \beta_1 \sum_{i=1}^t i + \sum_{i=1}^t u_t \end{aligned}\) | \(t \beta_0 + \beta_1 \sum_{i=1}^t i + y_0\) | \(t \sigma^2\) | Long | ||

| Random Walk w/ drift and non-deterministic trend | Non-Stationary | Same as above, but \(\beta_1\) is non-deterministic |

Impulse Response Function of covariance stationary process \(y_t\) is $$ \begin{aligned} \text{IR}(j) &= \dfrac{\partial y_t}{\partial \eta_{t-j}} \ &= \psi_j \ \implies \sum \text{IR}(j) &= \phi(L), \text{with L=}1 \ &\text{ (L is lag operator)} \end{aligned} $$

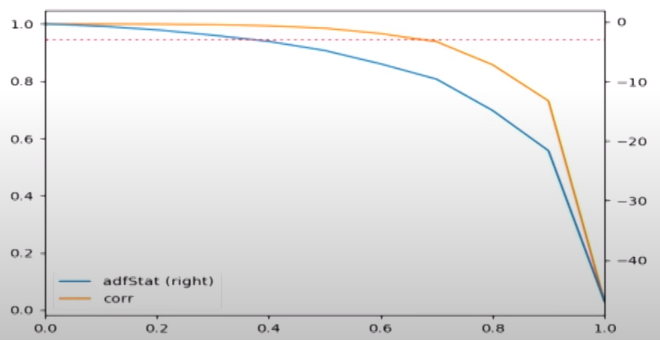

Differentiation¶

When converting a non-stationary series \(y_t\) into a stationary series \(y'_t\), we want

- Obtain stationarity: ADF Stat at 95% CL as \(-2.8623\)

- Retain memory: Similarity to original series; High correlation b/w original series and differentiated series

| \(d\) | Stationarity | Memory |

|---|---|---|

| 0 | ❌ | ✅ |

| \((0, 1)\) (Fractional differentiation) | ✅ | ✅ |

| 1 | ✅ | ❌ |

Integrated/DS Process¶

Difference Stationary Process

A non-stationary series is said to be integrated of order \(k\), if mean and variance of \(k^\text{th}\)-difference are time-invariant

If the first-difference is non-stationary, we take second-difference, and so on

Pure random walk is DS¶

Random walk w/ drift is DS¶

TS Process¶

Trend Stationary Process

A non-stationary series is said to be …, if mean and variance of de-trended series are time-invariant

Assume a process is given by

where trend is deterministic/stochastic

Then

- Time-varying mean

- Constant variance ???

We perform de-trending \(\implies\) subtract \((\beta_0 + \beta_1 t)\) from \(y_t\)

If

- \(\beta_2 = 0\), the de-trended series is white noise process

- \(\beta_2 \ne 0\), the de-trended series is a stationary process

Note Let’s say \(y_t = f(x_t)\)

If both \(x_t\) and \(y_t\) have equal trends, then no need to de-trend, as both the trends will cancel each other

Unit Root Test for Process Identification¶

| \(\textcolor{hotpink}{\beta_1}\) | \(\gamma\) | Process |

|---|---|---|

| \(0\) | White Noise | |

| \((0, 1)\) | Stationary | |

| \([1, \infty)\) | Non-Stationary |

Augmented Dicky-Fuller Test¶

- \(H_0: \beta_1=1\)

- \(H_0: \beta_1 \ne 1\)

Alternatively, subtract \(y_{t-1}\) on both sides of main equation

- \(H_0: \gamma=1\) (Non-Stationary)

- \(H_1: \gamma \ne 1\) (Stationary)

If p value \(\le 0.05\)

- we reject null hypothesis and accept alternate hypothesis

- Hence, process is stationary

We test the hypothesis using Dicky-Fuller distribution, to generate the critical region

| Model | Hypotheses \(H_0\) | Test Statistic |

|---|---|---|

| \(\Delta y_t =\) | ||

Long memory series¶

Earlier past is as important as recent past

Q Statistic¶

Test statistic like \(z\) and \(t\) distribution, which is used to test ‘joint hypothesis’

Inertia of Time Series Variable¶

Persistance of value due to Autocorrelation

Today’s exchange rate is basically yesterday’s exchange rate, plus-minus something